The net amount of cash that flows in and out of business is termed as cash flow. The cash flow largely depends on business activities in operations, purchases, and payments.

The cash flow efficiency of a business is determined by the working capital management, inventory management, and payment and collections process of a business. Cashflow-based lending by Banks and financial institutions is more efficient and safer than traditional lending against assets. However, Banks today still lack the tools to assess the drawing power of a borrower.

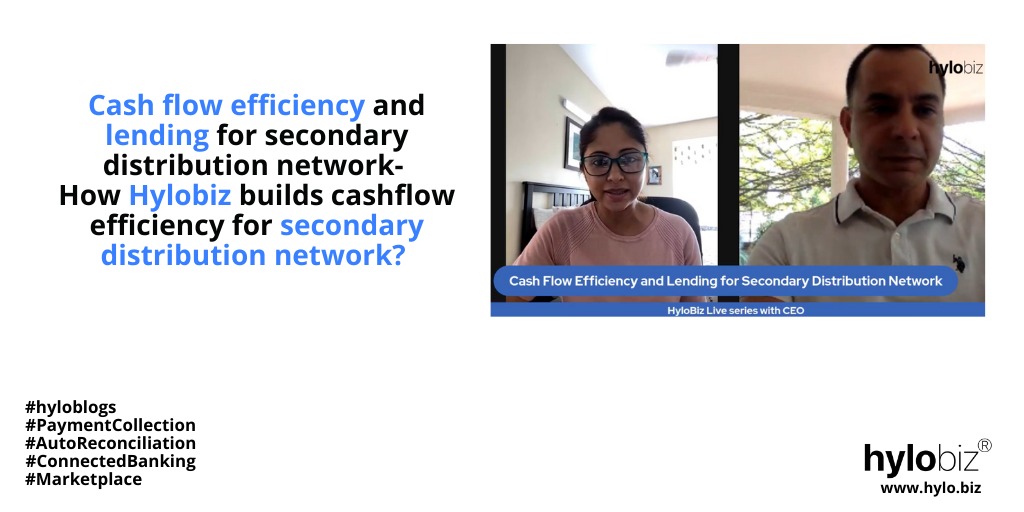

On 17th March, Hylobiz had a live Facebook session on “How Hylobiz builds cashflow efficiency for secondary distribution network?” Our CEO, Mr. Vishal Gupta, and Chandrama from the Technical team discussed, where Vishal explained every detail on cash flow efficiency and lending in connection to the secondary distribution network and how Hylobiz contributes to this.

Chandrama initiated the discussion where she said,

Hylobiz has come up with a solution that primarily intends to help SMEs with their payment and cashflow-related issues. The platform that Hylo offers is a simplified tool to basically automate all the payment-related activities with a primary focus on digitizing receivables.

[Chandrama] Who are the target SMEs we are talking about?

[Vishal] SME is a plant, a big manufacturer, and a big brand. An SME is a wholesaler and a distributor who buys from these guys, and then there are a lot of sub-dealers, traders, stockists, and then finally there are retailers from whom people like you and me as end consumers buy. So, there is a whole chain of SMEs and in this value chain, each of these SMEs has very different specific requirements when it comes to automation, connected banking, procure to pay cycle, visibility to inventory, access to capital, and stuff like that. So, from Hylobiz’s perspective, we were very clear that we wanted to stay in the mid-segment not really right at the top wherein you are talking about the big brands … the void that we saw is largely in the middle segment … that is, where we saw the working capital efficiency were required and to automate the working capital payout cycle and …this mid-segment was already sitting with a certain set of digital tools… the key very tactical for us was that their existing business tools were seamlessly connected to the banking platform. We are talking of the mid-segment SMEs.

[Chandrama] What are the challenges faced by SMEs?

[Vishal] The challenge is large because of manual broken processes where Tally does not fit to the collection system, the collection system does not fit to the banking system, the accountants update in Excel, the business owner is looking for information in the bank statement and nothing reconciled. Other than this the inventory status, which vendor to pay out when, how much to pay out to rotate their inventories, and stuff like that, access to working capital is a huge challenge. Lenders and underwriters find it tough to lend to this segment because of the broken set of information.

[Chandrama] What are the solutions the SMEs use?

[Vishal] There are new age ERP systems that have automated reminder processes were in automation on collections and reminders, some of them have integrated with the payment links, they look at NBFCs or the Fintech lending companies which are the new age lenders, to lend money to them, provide them working capital access, there are various invoice discounting companies, there are many Fintech companies who lend specifically focused to SMEs. The digital storefronts, and there are solutions which are available in the market, which we see that the SMEs are using today but they are still broken solutions…

It was clear from Vishal’s explanation,

Hylobiz can support in providing a single view of procurement, payment and collections to SMEs and based on this data, an SME business owner can enjoy faster capital access.

[Chandrama] How cash flow efficiency is important in secondary value chain?

[Vishal] (Vishal explained this with an example saying) How quickly am I able to rotate the money in a capital market is a direct factor of how quickly a bigger brand can do business with me. If I sell faster, I collect my money faster, I will go back and place my fresh order. This is something which is not visible to the brands today and they are keen to get to the visibility as what are the challenges of secondary sales today… the challenges are largely collection cycles are longer, the working capital is longer, information is broken, lot of manual processes in chasing the buyer to collect the money at distributor level… brands would want to see the secondary sales network cash flow efficiency to improve.

[Chandrama] Would you elaborate the term cashflow based lending?

[Vishal] When you are in a business there is a historical data to your invoicing, your payouts… there are lot of information around the aging of your collections, time of collections, what amount really get collected, what are the defaults out of these collections…it’s your actual cash flow within the business… This whole information once it is visible to a lender or a underwriter, with this whole transaction history, they are able to assess the risk more closely as compared to looking at the traditional ways of CIBIL score or your rating with the bank, or the amount of money you keep with the bank…risking or lending money to someone based on the day to day transactional data… With time, the situations have evolved, and the demands are for more real time transactions and more real time disbursements…and that is how it gets connected ERP, connected banking, real time access of information. Cashflow based lending is moving towards a journey of becoming more real time with all the open APIs connect globally.

[Chandrama] How is the scene cashflow based lending wise and cash flow optimization wise in India and globally?

[Vishal] The MSMEs, Kiranas and neighborhood stores, businesses like khatabook, dukaan and OKcredits are trying to build very similar efficiencies in terms of cash flow optimization, collecting your money faster trying to give capital access to MSMEs faster…very similar model Hylobiz is doing in mid segment and some of the bigger players and the banks… the mid segment basically called for micro integrations which Hylobiz and few more companies like Libero in Europe did similar stuff with quickbook and few other ERPS integration and there are lot of examples from Accounts Receivable and Accounts Payable perspective in the US, Paymate is one such company which is present across multiple companies… overall landscape has changed with APIs from most of these partner institutions becoming a commodity now, optimization of the overall cash flows within these segments and riding on data in real time basis to make decision on cashflow base lending is gonna be a very very hot space, is spoken by everyone and RBI in India has done a few articles in past one year…

Chandrama concluded the session highlighting, that,

in a country where about 15 million SMEs contribute to apparently 40% of GDP, it is truly satisfying experience to be able to create a platform that can help the SMEs.

Click here to see the video ‘Cash Flow Efficiency with Hylobiz CEO Knowledge Series’ on Youtube.

Email us at: support@hylo.biz.